Due Diligence Considerations for Investing in the Energy Transition - Part 1

Solar and Hybrid Solar & Storage Platforms and Pipelines

-

August 15, 2022

Downloads Download Article

Download Article

-

DNV’s Energy Advisory team and FTI Consulting’s Power, Renewables and Energy Transition(PRET) practice have partnered to examine the state of play in the US renewables M&A market and offer insight into key due diligence considerations for potential investors.

This is the first piece in a three-part series exploring key due diligence considerations for proven renewable energy and adjacent technologies representing the majority of M&A activity, as well as for emerging technologies poised for investment growth in the coming years. The series will cover the following themes:

- Part 1: Solar and hybrid solar & storage platforms and pipelines

- Part 2: Operating projects and portfolios

- Part 3: Emerging and enabling technologies

Introduction

Last year was historic for global private investment in low carbon and renewable energy initiatives, and the United States set a record with $105 billion deployed. 1 Demand for ESG investments was strong as a result of supportive new policies, comparatively low renewables costs, and increasing corporate commitments to reduce climate impact. In addition, strategics continue to deploy capital in the space at a rapid clip which has benefitted the sector and accelerated the energy transition. 2 Burgeoning demand is driving fierce competition for assets in commercially proven technologies, while investment in emerging technologies is hampered by smaller deal sizes, supply chain issues and unknown risk profiles.

We continue to see major M&A activity in the commercially proven arena in both renewable operating assets and development platforms, 3 and expect this will comprise the bulk of deals in the near term. Emerging and enabling technologies and opportunities such as offshore wind, EV charging infrastructure, and transmission make up a small but interesting slice of the pie that is expected to increase going forward. Against this backdrop, buyers can expect to contend with stiff competition and premium asset pricing, especially when a deal aligns well with a specific buyer’s strategic or ESG goals.

Overall renewables investment and deal volume remain robust but have recently faced significant challenges in the form of restrictive federal trade policies, supply chain disruptions, and volatility in the broader energy market and global economy. Supply of wind, solar and storage components was negatively affected by COVID, labor and shipping container shortages, and availability and pricing of raw materials. Supply of solar components was further hampered by federal policy around tariffs and forced labor concerns in China, including the announcement in March by the U.S. Department of Commerce (DOC) that it would investigate additional import tariffs on solar modules components. Executive action by the Biden administration announced on June 6, 2022, provides a 24-month moratorium on new tariffs; however, the damage already inflicted on 2022 solar development and construction timelines has been severe, with some estimates indicating a 40%-50% reduction in expected annual install capacity. 4 High inflation, increases in interest rates and of the overall cost of capital, and steeply increasing natural gas prices — in part related to the Russian war in Ukraine — further complicate the energy landscape. In order to be successful within this environment, it is critical that buyers be targeted and efficient with due diligence, and gain an understanding of key value drivers within the tight time frames typically mandated by sellers.

Market Overview

Sales of solar development platforms have been a key theme in renewable energy M&A in recent years. Notwithstanding the current headwinds the industry is facing, we expect this trend to continue, albeit with a refined focus on pipeline quality and management track record. In addition, potential acquirers will need to account for often long interconnection queues, land constraints, solar resources, and complicated storage dispatch and revenue models when evaluating project pipelines.

Federal directives regarding imports that benefit from forced labor in China, along with the U.S. Department of Commerce AD/CVD tariff investigation announced earlier this year, have made the valuation process significantly more complex by exacerbating the supply chain, commodity price and infrastructure-related challenges that had already been confronting the industry. Equipment shortages and uncertainty have been compounded by the DOC investigation, and projected commercial operation dates must be considered for reasonableness in light of these developments. During the pandemic, deliveries of solar and storage project equipment were regularly delayed and, in some cases, developers had to accept significant equipment price increases to avoid having deliveries cancelled under supplier force majeure notices. The DOC tariff investigation had significantly increased the risk associated with equipment supply over the near term. However, on June 6, 2022, the Biden administration announced a series of executive actions, supported by communication by the DOC, that eliminated the prospect of new or retroactively applied solar module tariffs for a period of 24 months. At the time of publication, details of the executive action are still forthcoming, but announced measures will undoubtedly create more market price certainty and reduce constraints that have slowed solar and storage investment for the last several months.

Diligence Approach

The renewable energy M&A market continues to be robust as a result of high demand and availability of capital but has also grown more complex in light of supply chain, federal policy and global economic conditions. In our experience, successful buyers rely on commercial and technical due diligence of key value drivers at both the project and platform levels.

Development Projects & Pipeline Considerations

To vet pipeline quality, assess risk, and evaluate solar and hybrid solar & storage investment opportunities, it is critical to take the following characteristics into account:

- Key milestones: For late-stage development pipelines, the developer should have appropriately de-risked the underlying projects by securing interconnection rights, offtake with a creditworthy counterparty, required permits, bankable equipment supply, and a validated approach to ITC qualification. Soft commitments from potential financiers, including tax equity investors and creditors, can provide additional endorsement. In the current environment, and especially when evaluating mature development pipeline and underlying projects, due diligence around equipment supply, including date certainty and potential tariff risk, will be paramount.

- Rigorous assumptions: Likewise for mature development pipelines, the developer should base energy yield estimates on realistic assumptions for the long-term solar resource at the project location 5 and follow a rigorous and accurate assessment methodology to reduce the risk of long-term underperformance. DNV’s recent validation paper 6 provides more details on best practices for state-of-the-art solar energy assessments. Additionally, for a given project, engineering studies, equipment selection, and the operations and maintenance (O&M) budget should support the assumed degradation, battery cycles and associated augmentation, and expected useful life. As part of this analysis, extreme weather risk should be evaluated and mitigated, with insurance costs being budgeted for.

- Pairing considerations: When evaluating development pipelines with a storage element, it will be critical to assess and validate the use case and revenue model under consideration (e.g., ancillary services, capacity, other) and the economic viability of such an approach in a given market. Regulatory considerations will be critical, and the route to ITC qualification for the energy storage equipment will need to be carefully considered as investors evaluate potential upsides offered by the pairing of solar and storage.

- Congestion and curtailment risk: This should be evaluated for all projects to confirm that the revenue assumptions are reasonable based on the current and future transmission in the region and that scenarios are run to capture associated risk.

- Pipeline maturity: For early to mid-stage development pipelines, it is reasonable to expect a lesser overall level of maturity. Nevertheless, the developer should have performed the requisite environmental, constructability, extreme weather and interconnection studies on underlying projects — including estimating transmission upgrade costs, which can be a deal-breaker in some ISOs/locations. Additionally, a robust strategy should be in place for ITC qualification, and production assumptions should be validated as reasonable. Offtake agreements may remain unfinalized, though more advanced discussions will increase value. The earlier stage of such project pipelines allows for additional flexibility in procurement and with navigating the challenges posed by solar supply-chain constraints; however, these factors must be taken into consideration and planned for with mitigating measures and strategies.

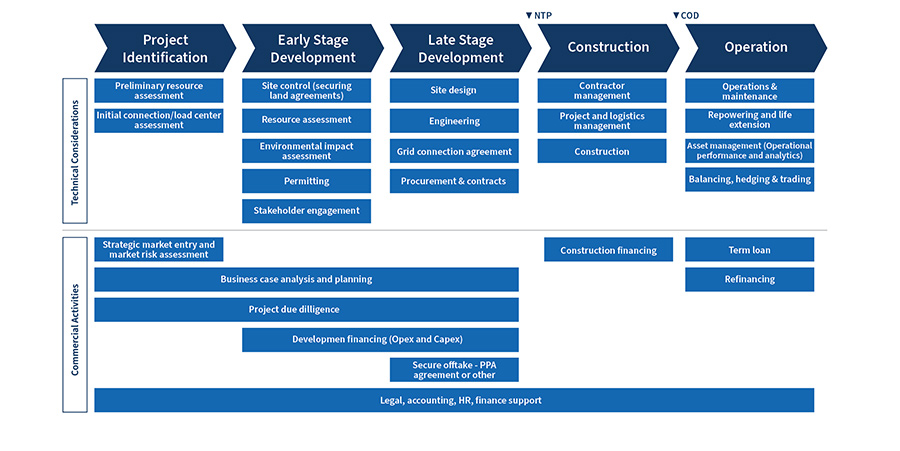

Exhibit 1: Illustrative Renewable Energy Project Development Process

Platform Considerations

In addition to the project considerations above, when considering platform acquisitions, potential purchasers also need to evaluate the capabilities, experience and scale of the development platform. Commercial and technical due diligence on a development platform is fundamentally an exercise in evaluating the experience and track record of the management team, maturity of processes and sophistication of the development approach, as well as financial health, resources and needs. Different developers have their own target markets and approaches, and may be focused on different development stages. For example, some developers focus on the early stage and sell projects well before they are shovel ready; others specialize in managing projects through construction and may even take an active role in operations. Each developer has a unique DNA, skill set and risk profile, and it is important that the acquirer’s due diligence process be tailored accordingly.

- Reputation: Management should demonstrate a strong record of bringing projects through the development cycle (see Exhibit 1). This is critical to establishing the credibility of the platform and the likelihood of success. Potential acquirers should also establish the full commitment of key members of management and staff following the transaction, and properly align incentives for future success through formalized retention plans and non-compete agreements.

- Business plan validation: The buyer should perform a thorough review and evaluation of the developer’s business plan, including growth prospects, financial assumptions and projections, and sources and uses of capital. It is critical to establish that the developer is on firm financial footing and that future capital needs are achievable and in line with the strategy of the potential acquirer. All business model assumptions must be validated, sensitized and adjusted, as appropriate.

- Development approach: There should be a well-defined and disciplined development process, with workstreams such as land control, permitting, interconnection and engineering having clearly defined stage gates before additional development costs are incurred. These processes limit sinking costs into projects that do not prove viable, thereby supporting the success of the overall pipeline as well as the valuation of the platform going forward.

- Key metrics: Analysis of success and mortality rates, development costs and margins at sale is important and enables benchmarking against the broader industry to evaluate a given platform’s competitive position within a consolidating landscape.

- Procurement approach: It is especially crucial in today’s market that a development platform has adequate mitigants and redundancy built into its procurement strategy. This can include master supply agreements, adequate safe-harbor capacity, and multiple supplier relationships. Despite the apparent easing of DOC tariff investigation impacts resulting from recently announced executive action from the Biden administration, we expect supply chain issues related to COVID, labor deficiencies and container shortages to persist into 2023. Where appropriate, potential acquirers may seek to mitigate associated risks – for example, through structuring earnout mechanisms.

Distributed Generation and Residential Solar Pipeline Considerations

Smaller distributed generation and residential solar energy pipelines typically comprise large volumes of relatively small projects. This composition makes detailed project-level diligence on the actual pipeline more cumbersome and less cost-effective. For these sub-segments, acquisitions are likely to take place at the platform level, and platform-level diligence should be the key focus. Review of sales and distribution models, relationships with buyers of projects, and health and safety risk become higher priority, whereas permitting and interconnection risk can be lower priorities. A higher-level, quantitative review of development feasibility and costs, capital expenditures, operating expenses, engineering assumptions and production benchmarking can be undertaken instead of the detailed, ground-up analyses used for utility-scale projects.

Summary

This year continues to be another busy one within the renewable energy M&A space, despite a more mixed array of market forces than those that drove record investments in 2021. Overall fundamentals of the asset class remain strong, and both market demand and availability of capital continue to drive deal flow. Supply chain challenges that began last year have worsened in 2022 and were exacerbated in the solar sector by federal trade and tariff policy. Global economic conditions have become less favorable, and tightening domestic monetary policy and increased natural gas prices create complexity for project development and investment.

Established technologies are likely to again represent the majority M&A activity, with solar and hybrid solar & storage development pipelines contributing significant volume. To increase the likelihood of success, prospective buyers should employ a targeted diligence approach with a refined focus on asset quality, management sophistication and track record.

Operating portfolio transactions will continue to make up an important part of market activity, and emerging technologies such as offshore wind and EV charging, as well as transmission infrastructure projects, are expected to represent an increasing portion of investment in the medium term. For a more detailed discussion of considerations related to operating renewable energy projects and emerging technologies, stay tuned for the upcoming releases of parts two and three of this series.

How We Can Help

DNV – Energy Advisory

Driven by our purpose of safeguarding life, property, and the environment, DNV enables organizations to advance the safety and sustainability of their business. We provide independent expert advisory, classification, technical assurance, and software services to the energy industry.

Combining leading technical and operational expertise, risk assessment methodology, and in-depth industry knowledge, we empower our customers’ decisions and actions with trust and confidence. Our expertise spans onshore and offshore wind power, solar, storage, transmission and distribution, smart grids, and sustainable energy use, as well as energy markets and regulations.

DNV has an unparalleled track record of providing technical support and innovation to the renewable energy industry. Our contributions include technology reviews, industry-leading risk assessment of major components, design of utility-scale solar projects, significant scholarship in the science of wind and solar energy assessment, and technical due diligence on an extensive range of projects. Learn more at www.dnv.com/energy.

FTI Consulting – Power, Renewables & Energy Transition (PRET)

FTI Consulting’s PRET practice helps clients across the value chain navigate the energy transition by providing a wide array of advisory services addressing the strategic, financial, operational, reputational, regulatory and capital needs of our clients. We provide tailored services for leading strategic and financial investors, assisting across all stages of the transaction life cycle, and have deep experience performing commercial, financial and operational due diligence on renewable energy platforms, projects and portfolios, on behalf of our clients.

In addition, through FTI Consulting’s wholly owned investment banking subsidiary, FTI Capital Advisors, we provide tactical strategic advice, buy- and sell-side advisory and capital-raising and have significant transactional experience in developing solutions and executing assignments in the U.S. capital markets for a wide variety of clients in renewables and adjacent sectors. As an independent investment bank, FTI Capital Advisors is free of conflicts, enabling us to provide clients with unbiased and uncompromising advice and execution capabilities.

Footnotes:

1: Henze, Veronika and Ben Finzel. “Record 2021 Investment, Demand Highlight Critical Role Sustainable Energy Technologies Play in the U.S. Economy.” Bloomberg NEF 2022. 2 “What is the Energy Transition Outlook.” DNV 2022.

2: “What is the Energy Transition Outlook.” DNV 2022.

3: “U.S. Renewable Energy M&A: Review of 2021 and Outlook for 2022.” FTI Consulting 2022.

4: “Solar Market Insight Report 2022 Q2.” SEIA 2022.

5: “Solar Resource Compass.” DNV 2022.

6: “Solar Energy Assessment Validation Study for Utility-Scale Projects.” DNV 2022.

Related Insights

Related Information

Published

August 15, 2022

Key Contacts

Key Contacts

Senior Managing Director, Leader of Power, Renewables & Utilities practice

Senior Managing Director

Senior Managing Director

Senior Managing Director

Managing Director