National Property Sector Overviews

-

September 14, 2022

Downloads Download Article

Download Article

-

Overall

- Rising interest rates will likely reduce spending (consumer and business) and result in lower investment activity.

- Operating expenses will rise.

- Higher expenses will impact tenants’ ability to absorb higher rents.

- The rising cost of construction will likely result in contracts or projects being delayed or cancelled.

- Despite numerous headwinds, investors still consider real estate a favorable asset to combat inflation as compared to fixed-income vehicles.

- Per the AFIRE 2022 International Investor Survey Report,1 U.S. commercial real estate will continue to be viewed as an attractive asset class by global investors.

- Although investors have amassed a large amount of capital to deploy, the gap between buyer and seller expectations will likely weigh on investment volume in select markets.

- Investors will continue to explore secondary and tertiary (smaller) markets, expanding property acquisition beyond core assets in gateway markets in the search for greater yields.

- Environmental, Social and Governance (ESG) in commercial real estate will continue to take on greater importance as more potential investors consider ESG when the assessing the long-term ability of an asset to attract quality tenants.

Office Market

- Market fundamentals have been mixed. Demand for space has weakened, resulting in a higher vacancy rate, driven by sublet space, which has increased 10% YoY.

- Net absorption rebounded in the first part of 2022 following several consecutive quarters of negative figures.

- Rent growth is now positive in most major markets.

- Investment sales activity has returned to pre-COVID-19 levels, driven by elevated demand for strategically located, stabilized trophy buildings.

- From September 2021 to August 2022, net absorption turned positive from the negative 87 million square feet recorded during the prior 12-month period.

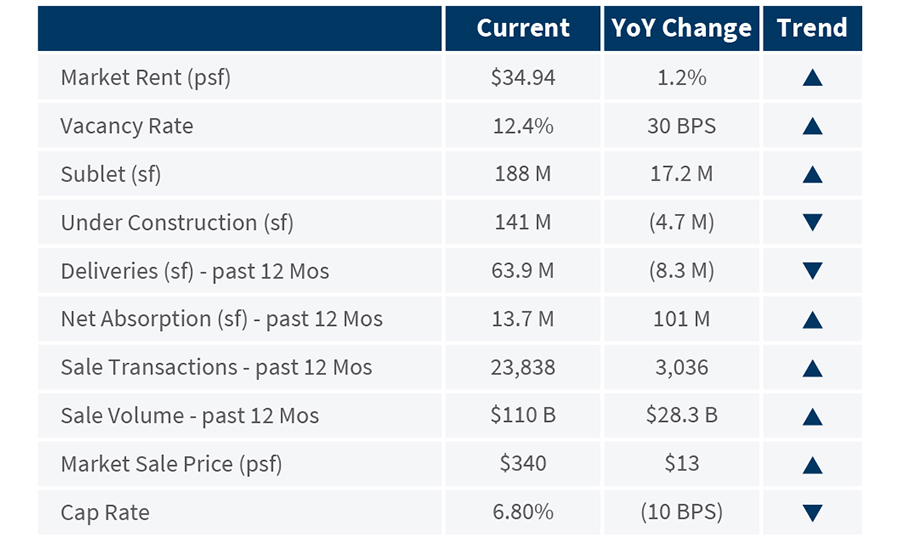

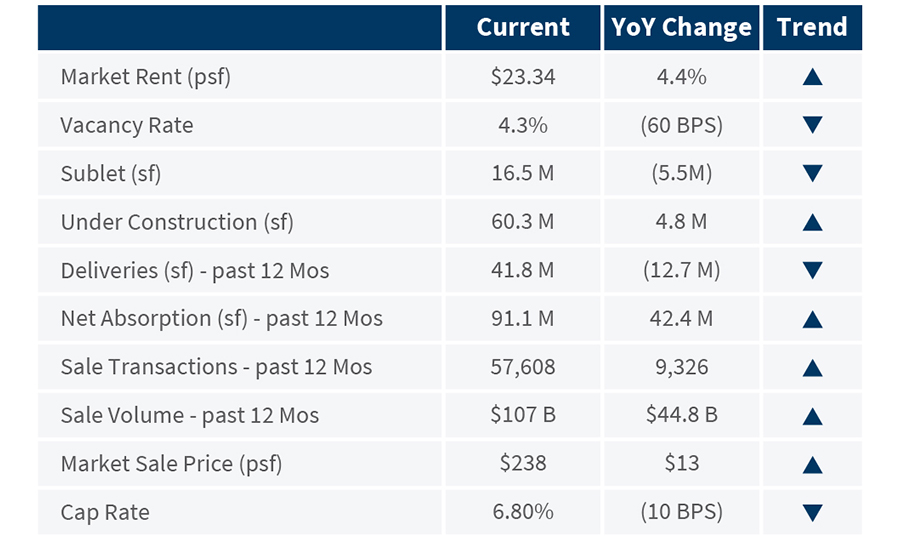

National Office Market Indicators

Source: Data compiled from CoStar (as of August 2, 2022).

Below are key metrics for the largest office markets in the United States:

10 Largest Office Markets (by Inventory) Comparison

Source: Data compiled from CoStar Office National Report - United States (August 2, 2022). 12 Mos - represents Sept. 2021 to Aug. 2022 period.

Source: Data compiled from CoStar Office National Report - United States (August 2, 2022).

Source: Data compiled from CoStar Office Capital Markets Report - United States (August 2, 2022). 12 Mos - represents Sept. 2021 to Aug. 2022 period.

Insights:

Office market recovery faces numerous headwinds.

- Hybrid work models and recession fears driven by aggressive Federal Reserve policy to combat high inflation have created uncertainty.2

- Office utilization is still a fraction of pre-pandemic levels and improvement has been slow.

- Firms will continue reevaluating their leases and square footage per employee, which was already shrinking before the pandemic.

- Although recent net absorption has been positive, weak demand from continuing space consolidation will put upward pressure on vacancy rates.

Industrial Market

- Market strength continues, characterized by record low vacancy rates, strong rental rate growth, and net absorption.

- Robust demand from logistics/big-box users and third-party logistics services (3PLs) seeking locations near strategic transportation linkages continue to place upward pressure on rental rates.

- A record influx of new development is occurring in attempts to satisfy strong demand.

- Investor interest remains healthy despite an uptick in commercial mortgage rates.

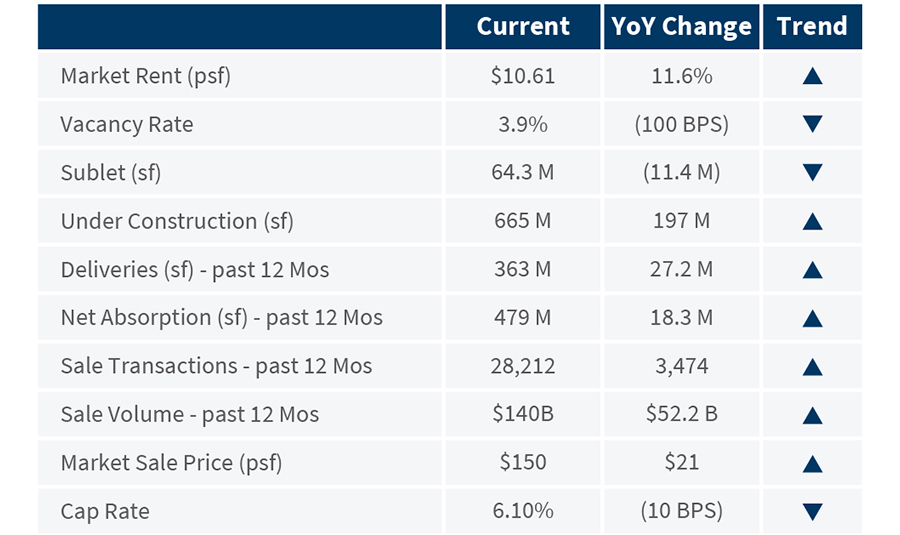

National Industrial Market Indicators

Source: Data compiled from CoStar (as of August 2, 2022).

Below are key metrics for the largest industrial markets in the United States:

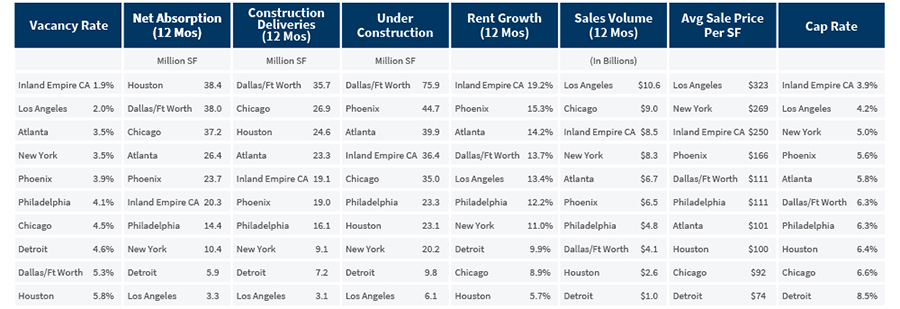

10 Largest Industrial Markets (by Inventory) Comparison

Source: Data compiled from CoStar Industrial National Report - United States (August 2, 2022). 12 Mos - represents Sept. 2021 to Aug. 2022 period.

Source: Data compiled from CoStar Industrial National Report - United States (August 2, 2022).

Source: Data compiled from CoStar Industrial Capital Markets Report - United States (August 2, 2022). 12 Mos - represents Sept. 2021 to Aug. 2022 period.

Insights

- In May, Amazon, the industrial market’s largest tenant, announced plans to sublease or vacate roughly 10 to 30 million square feet, raising questions about whether overall demand for industrial space may finally be cooling.3, 4

- Demand for warehouse space may moderate in the upcoming months due to reduced capacity needs from slower consumer spending.

- As vacancy rates in most of the nation's largest distribution hubs remain near historic lows, developers continue to seek developable land sites and available product in surrounding areas.

- Higher transportation costs, more integration of e-commerce, the onshoring of manufacturing, and the repositioning of global supply chains should boost long-term demand for industrial space.

- Investment may slow from its record pace set during the past 12 months, but buyer confidence in future industrial NOI growth remains high.

Multi-Family Market

- Record rent growth is moderating, but housing supply remains low in most markets.

- Demand is greater for relatively affordable units, where vacancy rates trend closer to 4.0%, in contrast to higher-end units, with vacancy rates upwards of 7.0%.

- Material shortages and supply chain disruptions have caused delays and raised the cost for new construction.

- Sales activity continues to outpace the other three major property types.

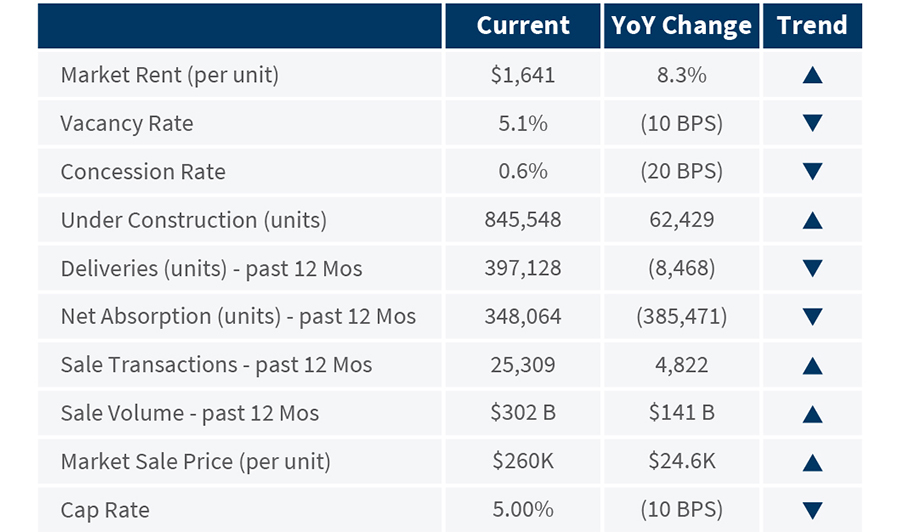

National Multi-Family Market Indicators

Source: Data compiled from CoStar (as of August 2, 2022).

Below are key metrics for the largest multi-family markets in the United States:

10 Largest Multi-Family Markets (by Inventory) Comparison

Source: Data compiled from CoStar Multi-Family National Report - United States (August 2, 2022). 12 Mos - represents Sept. 2021 to Aug. 2022 period.

Source: Data compiled from CoStar Multi-Family National Report - United States (August 2, 2022).

Source: Data compiled from CoStar Multi-Family Capital Markets Report - United States (August 2, 2022). 12 Mos - represents Sept. 2021 to Aug. 2022 period.

Insights:

- Market fundamentals are expected to remain strong due to favorable demographic drivers.

- Elevated levels of development will attempt to satisfy rental demand as high home prices and interest rates keep potential buyers in rental housing.

- Demographic trends show that the exodus from urban centers has slowed.

- Despite high costs, apartments incorporated into walkable, mixed-use developments and proximate to job centers and transit hubs continue to be favored by tenants.

- Heightened investment demand for multi-family assets is projected to keep cap rates near historical lows.

Retail Market

- Retail sales were unchanged in July 2022 from the prior month, largely due to declining gas prices and lower auto sales.

- Foot traffic at retail businesses has returned to pre-pandemic levels.

- During the past year, key metrics improved, due in part to limited new development.

- The majority of new construction consists of single-tenant build-to-suit projects.

- Sales volume totaled a record high since the Great Recession.

National Retail Market Indicators

Source: Data compiled from CoStar (as of August 2, 2022).

Below are key metrics for the largest retail markets in the United States:

10 Largest Retail Markets (by Inventory) Comparison

Source: Data compiled from CoStar Retail National Report - United States (August 2, 2022). 12 Mos - represents Sept. 2021 to Aug. 2022 period.

Source: Data compiled from CoStar Retail National Report - United States (August 2, 2022).

Source: Data compiled from CoStar Retail Capital Markets Report - United States (August 2, 2022). 12 Mos - represents Sept. 2021 to Aug. 2022 period.

Insights:

- Although consumer sentiment increased slightly in July 2022, it remains near all-time low levels amid concerns over inflation and an upcoming economic recession.5

- Besides inflationary worries, retailers continue to deal with headwinds such as labor shortages and supply chain disruptions.

- Leasing and rental growth will accelerate in markets with the strongest population growth, particularly in the Sunbelt and western regions.

- Investors will continue targeting single-tenant net lease assets and grocery-anchored neighborhood centers in high-growth areas.

- Repositioning and transforming older vacant retail assets into new, consumer-driven venues and mixed-use projects that feature more food, entertainment, and non-traditional tenants in the strongest markets will continue despite challenging conditions.

- Many retail centers in secondary and tertiary markets will remain vacant due to very limited demand for alternative uses.

How FTI Consulting Can Help

Whether you are an individual with a single asset or a multinational corporation or fund that controls asset portfolios located throughout the world, we apply our in-depth understanding of real estate transactions, values and market dynamics to advise you throughout the life cycle of ownership and in complex situations like bankruptcy, restructuring and disputes.

With real estate valuation professionals possessing the requisite combination of “expert witness” credentials, industry-recognized designations (MAI, CRE, FRICS and MRICS) and real-world transaction experience, we are well-positioned to provide advice and support to maximize client benefits.

Footnotes:

1: AFIRE 2022 International Investor Survey Report, The Association of Foreign Investors in Real Estate, underwritten by CBRE & Holland Partner Group (April 20, 2022), 2022 AFIRE/AFIRE.org.

2: Wiseman, Paul, Fed's aggressive rate hikes raise likelihood of a recession, Associated Press (June 16, 2022), Associated Press.

3: Soper, Spencer, Amazon Aims to Sublet, End Warehouse Leases as Online Sales Cool, Bloomberg (May 21, 2022), Bloomberg.com.

4: Kirk, Patricia, Amazon's Plan to Sublease Industrial Space May Just Be the Start, Wealth Management (June 9, 2022), wealthmanagement.com.

5: Fontdegloria, Xavier, U.S. Consumer Sentiment Remained Subdued in July; Inflation Expectations Fell -- University of Michigan, MarketWatch, Inc. (July 15, 2022), marketwatch.com.

Related Insights

Related Information

Published

September 14, 2022