Partnerships At Sea - A Developing Story In The U.S. Offshore Wind Market

The U.S. Offshore Wind Market Offers Attractive Investment Opportunities

-

November 29, 2021

Downloads Download Article

Download Article

-

The development of the U.S. offshore wind market has been driven by federal and state energy policies facilitating the procurement of contracted offshore wind capacity along the East Coast while also providing tax incentives as another mechanism to promote development. In March 2021, the Biden administration announced its plan to support and expand the development of offshore wind as a renewable energy source. As part of a $3 trillion economic recovery package focused on improving infrastructure and reducing emissions in the U.S., the Biden Administration set a goal to reach 30 GW of offshore wind turbines by 20301.

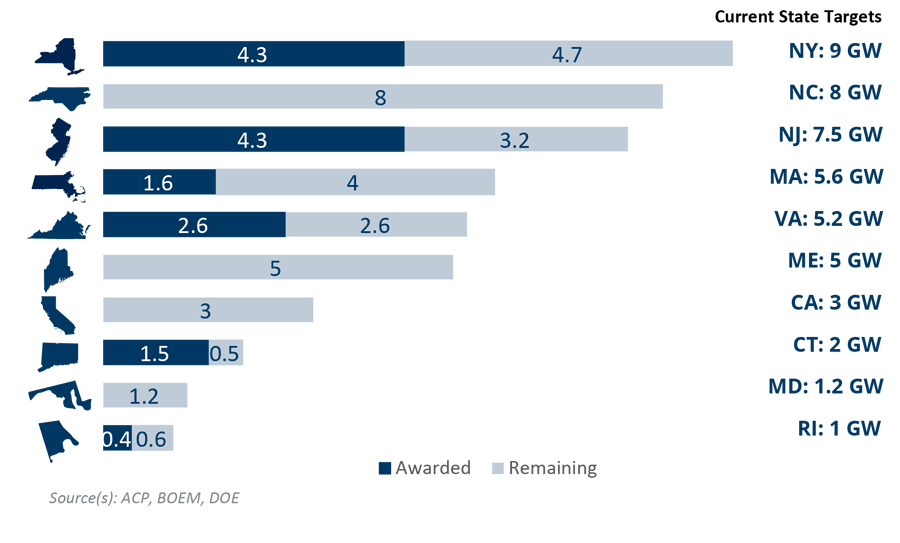

Since 2010, 10 East Coast states across the U.S. have publicly announced offshore wind targets, totaling nearly 50 GW of cumulative capacity, with incremental expansion expected in California and the Gulf of Mexico. As much as $70 billion2 of capital in aggregate will be needed to meet targeted installed capacity. Funding the amount of capital required to support the buildout will require new investors across the capital stack capable of writing significant debt and equity checks and with required return levels commensurate with the risks of the offshore wind investment3.

Figure 1 - Offshore wind targets by state total to 47.5 GW of capacity to be procured by 2040

The development of offshore wind farms presents both opportunities and challenges that are unique to the offshore space, relative to onshore wind projects.

Targeted returns for offshore wind projects are in the 7% - 8% range, on an unlevered basis, and while this is a lower return threshold than what is typically required in the oil and gas industry, the cash flow profile is far more stable and less risky. As with utility-scale onshore renewables in the U.S., the capital stack is likely to be comprised of a combination of project level debt, back-leverage, tax equity and sponsor equity.

While offshore wind does present a significant opportunity, potential investors should consider key challenges they may face, such as high technical barriers to entry, a complex supply chain and regulatory restrictions. The skills and expertise required to lay foundations, erect turbines, and lay subsea cables are extremely difficult to develop organically with only a select few boasting the capability. States will need to collaborate and foster a domestic supply chain without creating inefficiencies that raise the LCOE and effectively undermine the sector. The goal of promoting the advancement of offshore wind in the U.S. is to increase the technology’s reliability while lowering production costs.

Another hurdle affecting offshore developers in the U.S. is the Jones Act ― a maritime statute signed into law in 1920. The Jones Act requires all ships that deliver goods shipped between U.S. ports to be transported on ships that are built, owned, and operated by U.S. citizens or permanent residents. In response to the Jones Act, Dominion Energy, a utility based in Virginia, is leading a consortium of renowned naval engineering firms to build a $500m Jones Act-qualified vessel. In May of this year, a collaborative project between NREL, the State of Maryland, NYSERDA and the DOE was launched to develop a Supply Chain Roadmap which will present the collective benefits of a domestic supply chain and facilitate the acceleration of the offshore wind industry in the U.S.4.

Given the significant financial and technical barriers to entry, the competitive landscape has begun to crystallize into the three distinct categories of competitors: European offshore wind developers, major oil and gas companies, and U.S. electric utilities.

European offshore wind developers, such as the global market leader Ørsted, are perhaps the most obvious choice to lead the U.S. buildout of offshore wind given they can capitalize on expertise cultivated in more developed international offshore wind markets. In the U.S. alone, Ørsted has a development pipeline comprised of 4 GW of awarded capacity with another 3 GW in earlier stage projects5.

Oil & gas majors have identified offshore wind as an opportunity to leverage offshore oil and gas drilling expertise while “greening” their portfolios. Their expertise in developing and operating large offshore oil and gas projects can be leveraged as they seek to transform their business models and look to put this experience to work developing offshore wind projects at scale. Majors can adapt their approach and apply existing technologies to offshore wind applications, such as using existing rig infrastructure for power generation or operational facilities for offshore wind development. From a financial standpoint, oil and gas companies also have significant access to capital, scale and a strong balance sheet. Examples in the U.S. include Shell with a portfolio of 4.1 GW (2.3 GW awarded capacity) and 50% ownership across two seabed lease areas6, BP and Equinor which have formed a 50/50 partnership that has been awarded 3.3 GW of capacity and Total and EnBW who recently announced a joint venture focused on investment in the East Coast of the U.S.7.

U.S. electric utilities have the expertise in the country’s regional markets, regulatory compliance issues and onshore transmission to positively contribute to the development of offshore wind. Utility players also possess impactful stakeholder relationships and routinely engage in meaningful community outreach allowing them to facilitate momentum and streamline projects. Avangrid, a leading U.S. utility whose parent is global renewables ‘supermajor’ Iberdrola, has been awarded 1.6 GW of capacity in joint projects with Danish investor Copenhagen Infrastructure Partners. The two developers recently announced8 an agreement to restructure their jointly held 5.3 GW offshore wind portfolio and focus on their own expansion plans separately. Avangrid also has a 2.5 GW project in development off the coast of North Carolina9. Eversource is one of the nation’s utilities leading the development of offshore wind throughout the Northeast with over 4 GW of total development pipeline in partnership with Ørsted10. Also, with Ørsted, PSEG is increasing its stake in the space in coordination with New Jersey’s goal of 50% clean energy and 100% renewable power by 2050. Finally, French utility EDF is an example of a European utility that is a major player in U.S. offshore wind, having been awarded 1.5 GW offtake out of a potential 2.5 GW in its Atlantic Shores project jointly owned with Shell.

Entering the market alone can be done, but it will be a challenging road accomplished by few experienced players.

The first critical step for companies seeking to invest in U.S. offshore wind is to evaluate their core in-house competencies and the capabilities that must be developed or acquired to be competitive in offshore wind solicitations and determine whether to complement their existing skill set either organically or through acquisition. There is a limited amount of offshore seabed where wind farms can be economically developed and as a result a finite opportunity set to invest in. As much as 35 GW could be developed on the East Coast through 2050. New entrants will need to have or quickly obtain the requisite technical, market and commercial expertise to monetize the opportunity. Where this expertise is lacking, joint ventures or acquisitions will be a more expeditious means of filling gaps than organically building the necessary competencies as Ørsted did nearly a decade ago.

Given the time constraints associated with organic transformation, joint ventures or acquisitions are another option for standalone players looking to enter the U.S. offshore wind market. Investors who have available capital could acquire development assets on the secondary market. Investors will need to perform meticulous due diligence on available assets and projects to ensure they align with their skill set and risk tolerance. Even Ørsted has pivoted away from the standalone strategy: between 2020 and 2027, Ørsted expects a growth in operating profit (EBITDA) from offshore and onshore assets in operation of approximately 12% a year on average, reaching a level of DKK 35-40 billion in 2027. The growth rate assumes that all offshore projects where Ørsted does not already have a joint venture partner are farmed down to a 50% ownership stake11.

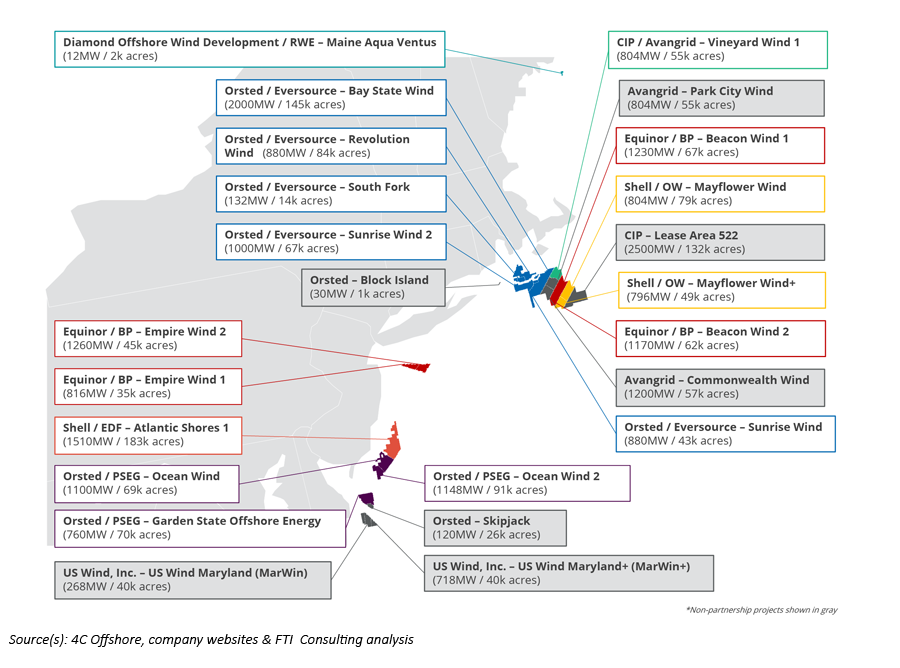

The unique expertise required to be successful in a state solicitation has meant that except for a select few European developers, almost no participants exclusively hold the requisite technical expertise, commercial expertise and financial strength to bid independently. Instead, the market has seen a shift towards critical partnerships developing where companies are seeking to pair their core competencies to synthesize a more compelling offering for regulators to evaluate. Figure #2 above highlights partnerships’ predominance over standalone ownership throughout East Coast lease areas.

The traditional power players in offshore wind have been targeting partnerships with two distinct types of companies as they look to increase their U.S presence: oil & gas majors and U.S. electric utilities. Oil & gas majors draw on technical expertise, strong supply chain relationships, construction expertise and financial strength. The expertise, infrastructure and local market knowledge of global oil and gas players already operating in capital intensive markets has scaled up. BP invested in Equinor’s U.S. offshore wind assets partly to build technical competences in the area. As the seller, Equinor has experience in offshore wind but sees value in its partnership with BP on other levels, such as. BP’s knowledge of the U.S. offshore environment and power markets. Equinor highlighted the value of teaming up with like-minded oil majors with progressive climate agendas. Its farm-outs to BP and ENI can lead to collaboration in other areas of the energy transition such as hydrogen and carbon capture, utilization and storage (CCUS)12. Shell has partnered with Ocean Winds (a joint venture between EDP Renewables and ENGIE) on two Mayflower Wind projects (potentially 1.6+ GW) and with EDF Renewables on the Atlantic Shores project with a capacity that could reach up to 2.5 GW. The Mayflower Wind projects ultimately combine the experience of two major types of players, utilities with offshore wind experience and oil and gas, to deliver a strong auction bid and gain scale in the offshore wind space.

Developers have also partnered with U.S. electric utilities to leverage the utilities’ commercial savviness and strong relationships within U.S. markets and communities. Ørsted established partnerships with PSEG and Eversource to develop projects with a combined capacity of approximately 5.9 GW. Both utilities hold critical institutional knowledge of the onshore transmission grid and key stakeholder relationships to facilitate the commercial development of OSW projects. Ørsted and Eversource’s agreement to charter Dominion Energy’s Charybdis is the first Jones Actcompliant installation vessel in the U.S. and will enable the construction of two wind farms that are expected to be seaready by late 2023. This will also mark a major milestone in the offshore wind industry, expanding the possibility for U.S. local supply chain development and reducing reliance on global sourcing challenges 13.

Partnerships are often the best way to facilitate a successful entry for a successful entry into the offshore wind market.

As the industry becomes more and more global, players are forging alliances to tap into synergies, but know-how and relationships within the U.S. market are undoubtedly a key to success. Partnerships are not without challenges. Identifying the right partner, effective integration, agreement on an equitable split of resources, intellectual property and financial returns or obligations all present complications in trying to develop a successful proposal in a timely and resource-efficient manner. Those headwinds aside, partnerships are the preferred approach for a new market entrant given the finite timeline and unique set of required skills. So far, none of the oil & gas majors are developing a U.S. offshore wind farm alone or with a U.S. domestic partner. For the majors, partnering with offshore wind companies seems like a clear advantage, but it can also present cultural challenges when these dynamic forces come together. The key is to maintain a balance when evaluating the alliance, not overstating synergies, and acknowledging differences that can lead to friction.

Offshore wind in the U.S. is a budding market ripe with opportunities for companies capable of overcoming the significant barriers to entry. Successful market entry is predicated on a thorough evaluation of the competitive landscape and identification of the right partnership that meets both parties financial, commercial, and strategic goals. Players that can successfully penetrate the market will have the ability to deploy significant capital at attractive risk-adjusted returns. However, it is critically important that investors are making well-informed investment decisions and are targeting the appropriate opportunities, at the right valuations, while understanding the financial, economic, market and commercial risks of each project.

Footnotes:

1: Friedman, Lisa, and Brad Plumer. “Biden Administration Announces a Major Offshore Wind Plan.” The New York Times, The New York Times, 29 Mar. 2021, www.nytimes.com/2021/03/29/climate/biden-offshore-wind.html.

2: ACP. (2021, January 19). New report: U.S. offshore wind generates $70 billion supply chain opportunity. American Clean Power, from https://cleanpower.org/blog/new-report-u-s-offshore-wind-generates-70-billion-supply-chain-opportunity/.

3: McClellan, Stephanie. “Supply Chain Contracting Forecast for U.S. Offshore Wind Power.” Special Initiative on Offshore Wind, Mar. 2019, https://www.noia.org/wp-content/uploads/2019/05/SIOW-Paper.pdf.

4: Gerdes, Justin. “Building Out the U.S. Offshore Wind Supply CHAIN-A $68 Billion Opportunity.” Building Out the U.S. Offshore Wind Supply Chain -- a $68 Billion Opportunity | Greentech Media, Greentech Media, 22 Apr. 2019, www.greentechmedia.com/articles/read/building-out-the-us-offshore-wind-supply-chain-a-70-billion-opportunity. “What Can the U.S. Offshore Wind Market Learn from Europe?” Arp, www.arup.com/perspectives/us-offshore-wind-market.

5: Ørsted company website as of 4 October 2021, https://us.orsted.com/wind-projects

6: Shell company website, as of 4 October 2021, https://www.shell.com/energy-and-innovation/new-energies/wind.html

7: https://totalenergies.com/system/files/documents/2021-09/2021_TotalEnergies_Strategy_Outlook.pdf

8: Avangrid and CIP press releases, 21 September 2021, https://www.avangrid.com/wps/portal/avangrid/pressroom, https://cipartners.dk/category/press-release/

9: Avangrid company website as of 4 October 2021, https://www.avangrid.com/wps/portal/avangrid/sustainability/technologyandinnovation/offshorewind

10: Eversource company website as of 4 October 2021, https://www.eversource.com/content/general/about/sustainability/focus-areas/renewable-generation

11: Reve. “Orsted Accelerates Growth to Realize Its Full Potential as a Global Wind Energy Major.” REVE News of the Wind Sector in Spain and in the World, 2 June 2021, www.evwind.es/2021/06/02/orsted-accelerates-growth-to-realise-its-full-potential-as-a-global-wind-energy-major/81061.

12: “Why Offshore Wind Is Proving So Attractive to Oil and Gas Companies.” NS Energy, 8 Apr. 2021 www.nsenergybusiness.com/features/oil-companies-offshore-wind/.

13: “Ørsted, Eversource to Charter U.S. FIRST JONES Act-Compliant Offshore Wind Turbine Installation Vessel.” Offshore Engineer Magazine, 1 June 2021, www.oedigital.com/news/488083-rsted-eversource-to-charter-u-s-first-jones-act-compliant-offshore-wind-turbine-installation-vessel.

Related Insights

Published

November 29, 2021

Key Contacts

Key Contacts

Senior Managing Director, Leader of Power, Renewables & Utilities practice

Senior Managing Director

Managing Director

Managing Director